Solar Financing…

No bucks, no Buck Rogers

No solar project, no matter how big or how small, can take place without the availability of financing.

Paraphrasing The Right Stuff:

“You know what makes your projects fly? Funding. No bucks, no Buck Rogers.”

While cash is, was, and always will be king, for many potential solar clients a cash purchase is just not in the cards. Unfortunately, that has led to the growth of some financing methods—like residential leases—that are a great deal for the finance companies, but not such a great deal for the consumer.

Beyond financing methods, rebates and tax incentives are key in determining the profitability of going solar!

Residential Financing Solutions

Residential Solar Loans—the User-Friendly Alternative to Leasing

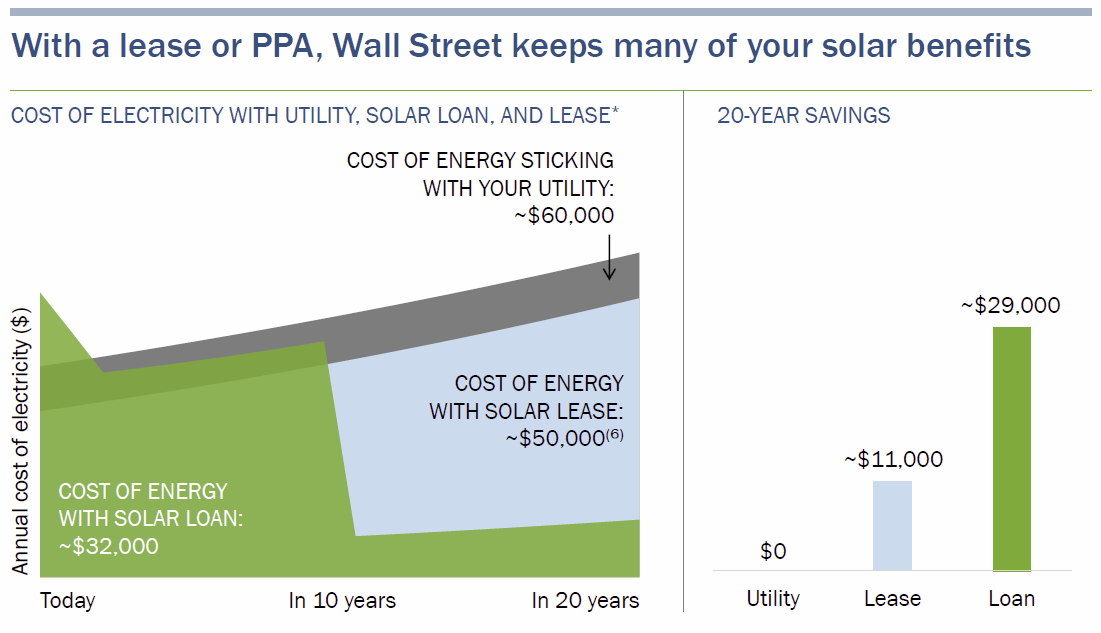

Although leasing has gotten a lot of buzz when it comes to financing residential solar projects, the simple truth is that such programs are often a poor choice for the consumer. As the graph below shows, a solar loan could save you nearly three times as much money over twenty years as you would leasing the same system.

Click for larger image.

So what else aren't the financing companies telling you about leasing? Well…

- The leasing company will pocket both your rebate and the federal tax credit.

- A lease may make it more difficult to sell your home—will prospective buyers qualify for the lease, and will they want to assume that obligation?

- Leases (and especially PPAs) often include escalator clauses that increase your costs every year. If utility costs increase at a slower pace, you could actually lose money.

- Need more? We put together a list of the Top Five Reasons to Avoid a Solar Lease!

Talk about a buzz kill!

Financing your solar project through a loan, on the other hand, lets you keep both the rebate and the tax credit. Depending on your personal credit status, there may be several loan options available to you, including:

- Home Equity Line of Credit—If your credit score is high, and you have equity in your home, chances are that a home equity line of credit (or HELOC) may be your best option, providing the lowest possible interest rate and the most favorable terms overall. Check with your local bank or credit union.

- Solar-Specific Loans—Companies like Mosaic are offering loans specifically tailored to solar projects. You can re-amortize the loan without cost, which allows you to apply those incentives to your loan balance, thereby reducing your monthly payment. Loan terms range from 5 to 20 years, and interest rates vary depending on the loan terms and your FICO score.

We are very excited about solar loans for clients who cannot afford to purchase their system outright. Before you sign on the dotted line for a lease, we urge you to give us a call and let's see if a solar loan on a Run on Sun solar system can save you some serious money.

Property Assessed Clean Energy (PACE) Financing for Residential Solar through HERO

PACE financing for residential projects has become a viable option, thanks to the creation of the HERO (Home Energy Renovation Opportunity) program that began in Riverside county. Now the HERO program has expanded into Los Angeles and Orange counties (amongst others).

The HERO Financing Program provides homeowners a unique opportunity to make home energy improvements through property tax financing. Because the load is tied to the property, it is not dependant on the homeowner's personal credit score. Rather, as long as the property taxes are current and no bankruptcy within the past two years.

Benefits include 5-20 year terms, tax-deductible interest, transferability when the property is sold and consumer protections.

The HERO program launched in Los Angeles County on May 23, 2014 with just a handful of cities. Since that time, the program has expanded dramatically, and now includes more than 100 cities in LA and Orange counties.

Based on the HERO website, here's a list of the participating cities as of January, 2016:

Click to see if your city participates in HERO…

Close